If you are having trouble understanding your insurance claims for damage that has occurred to your property, you're not alone! Insurance documents can be confusing. There are a bunch of terms and many of them don't make any sense on this form, there are a bunch of sections that don't seem to relate to anything meaningful, and there you may be aware of the endless array of dollar amounts and they oftentimes don't seem to add up.

This blog aims to support you during your claims process. It will provide you with a step-by-step guide on how to read your insurance claim document so that you can understand what is being covered and what isn't. We'll also provide some tips on what to do if something doesn't make sense.

Why All Insurance Claim Documents Look The Same

About 90% of insurance companies and adjusters use the same software program to create your property insurance claim estimate. The program is called Xactimate. There are different ways that an adjuster can set up the Xactimate program and templates, and each way will make the document look a little different, but basically, they'll all be the same.

The first page will most likely have the information about your insurance company, the name and contact info for the adjuster, and your claim number, and policy number. It will also have your name and contact info. Many insurers will also put a complete summary of the damages on the first page as well.

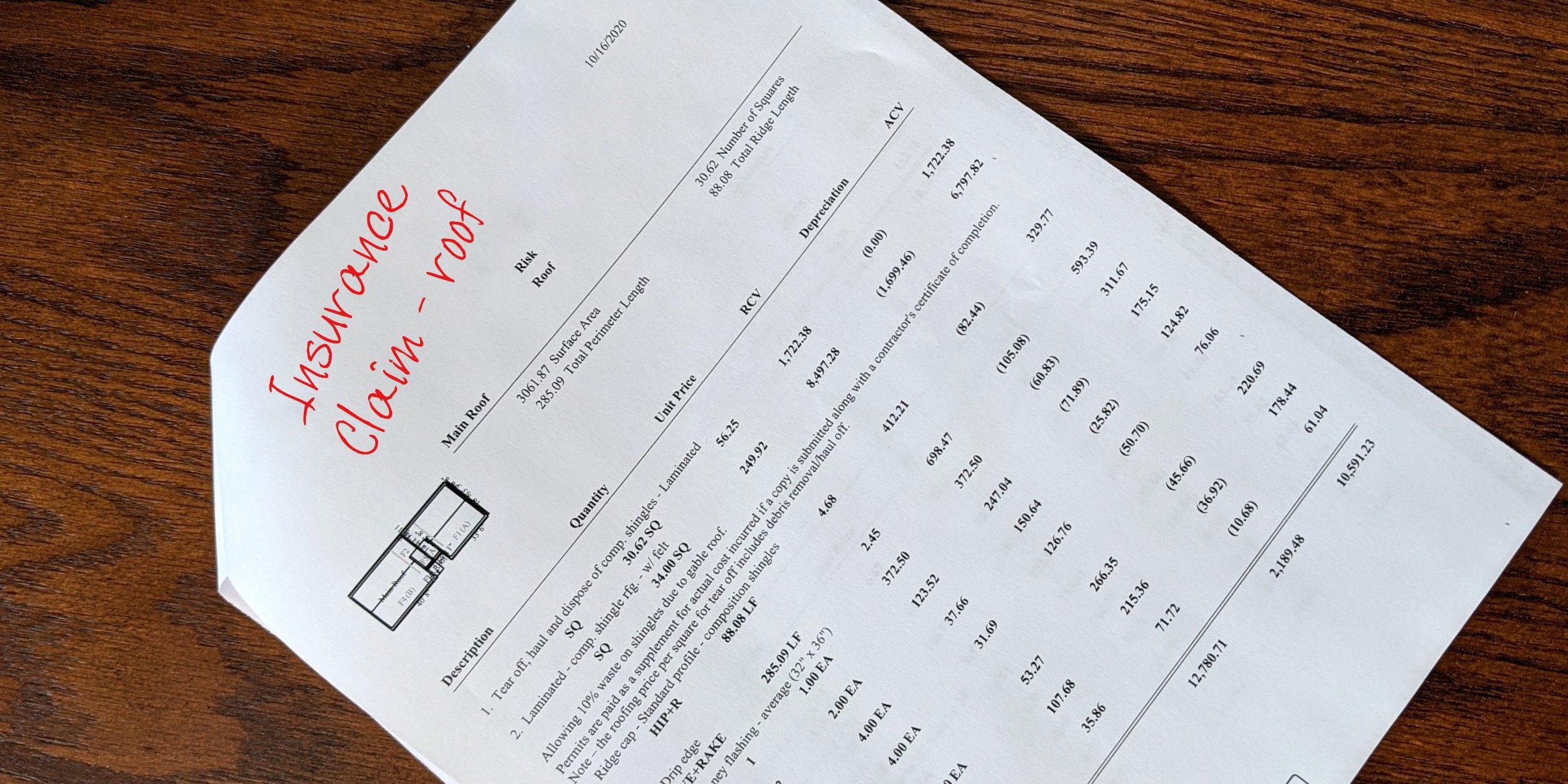

The first page is important, but it's not where you're going to find the details of what was damaged and how much it will cost to replace or repair or the estimate of roofing materials. For that, you'll need to look at the next few pages for that additional information.

More importantly, it will have the "30,000-foot view" of the claim, meaning, you'll see the bottom-line dollar amounts associated with your claim. You'll see the full claim amount (Replacement Cost Value), the amount of the depreciation, your deductible, and the net claim, or actual cash value amount. Here's what each of those terms means:

Replacement Cost Value

This is the total amount that your insurance company has estimated as the cost of repairs to your property.

Depreciation

Your insurance company will apply depreciation to your damaged property based on the age and the "life expectancy" of the product. So if you have a "30-year" shingle on your roof, and its current age is 15 years, then your roof is 50% depreciated.

Deductible

This is your share of the cost of the repairs. Legally, this amount is your responsibility to pay. It cannot be paid or discounted by your contractor.

Actual Cash Value (aka Net Claim)

This is the amount that your insurance company is giving you at the start of the claim. This is the Replacement Cost Value minus the depreciation and minus the deductible.

There are a couple of other important terms. These are actually VERY important!

Recoverable Depreciation

If your claim has recoverable depreciation, that is money you will receive after you have incurred the costs for the repairs. If you have Replacement Cost Value coverage in your policy, your depreciation should be "Recoverable." This is a policy that is generally more cost-effective.

Non-Recoverable Depreciation

If your insurance coverage is Actual Cash Value, then the amount of the depreciation will be Non-Recoverable. This means that you will not receive the depreciation amount as part of the claim. So, if you only have Actual Cash Value coverage, your share of the cost of repairs will be much, much higher than if you have full Replacement Cost coverage. You should definitely know which coverage type you have before filing an insurance claim.

Another important piece of information on the front page of your claim is a code that refers to the Xactimate price list that your adjuster is using. This code indicates the city or area your property is in and a month and year. Xactimate updates or revises material and labor pricing in its program every month. This can have either a small effect or a very large effect on the amount of your claim.

For example, if your property gets damaged by a storm in May, but you can't get the repair work done until September, if material and labor pricing is different in September, that will affect the actual cost of repairs you will incur.

We're dealing with a dramatic difference in a claim right now. A homeowner filed a claim for hail damage a few days ago, but the adjuster created his claim document using a Xactimate price list that is a year old. He did this because the storm that damaged the house happened a year ago. There have been about 6 price increases in roofing materials in the last year, so the claim is substantially too low.

Obviously, a contractor can't go back in time and buy roofing materials at the price they were a year ago, so the adjuster will need to revise his claim document to use the most current price list.

There are many more details involved in understanding your claim document, but for now, this will give you a start on clarifying the information on the front page.

________________________________________________________________________________

Homestead Roofing has inspected, repaired, and replaced thousands of roofs in Colorado Springs and the surrounding counties.

As a family-owned business, we take every project personally, committing all our efforts and expert advice to ensure you and your loved ones have an excellent roof for your living space. Contact us today for more information about our roofing solutions.